Can You Retire Comfortably in India? Central, State & Private Pension Schemes Compared 2026

Cross-referencing the PFRDA scheme registry against the Department of Financial Services portal in April 2026, one fact is jarring: India now runs more than 10 distinct pension frameworks simultaneously — from the Unified Pension Scheme for 2.3 million central government employees to the ₹42-a-month Atal Pension Yojana for gig workers, to private annuity products from LIC, HDFC, and ICICI Prudential promising lifelong income. Most Indians are enrolled in exactly one of these — often without knowing whether it is the right one for their income type, age, or risk appetite.

Here is what nobody tells you upfront: the best pension scheme in 2026 depends entirely on who you are — not which scheme has the biggest subscriber numbers. A central government employee choosing between UPS and NPS faces a permanently irreversible decision. A private-sector worker who never joins EPS loses a pension they have already earned rights to. An unorganised worker choosing between APY and PM-SYM is picking between two government-guaranteed schemes that cannot be held simultaneously. This article cuts through the noise — every major scheme, three sectors, one verified 2026 framework.

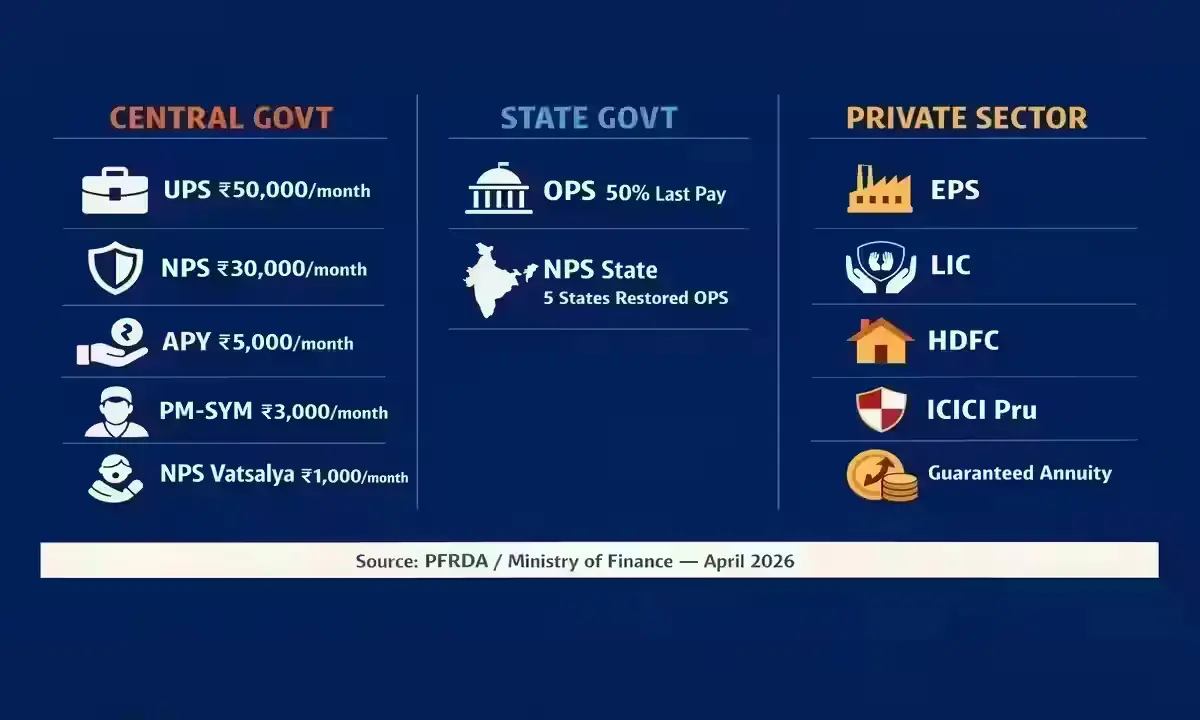

| Central Government 5 Active Schemes UPS • NPS • APY • PM-SYM • NPS Vatsalya | State Government 2 Frameworks OPS (5 states) • NPS (all other states) | Private Sector 3+ Options EPS • LIC Jeevan Shanti • HDFC • ICICI Pru |

PENSION LANDSCAPE 2026

- India operates 10+ active pension frameworks across Central, State, and Private sectors as of April 2026.

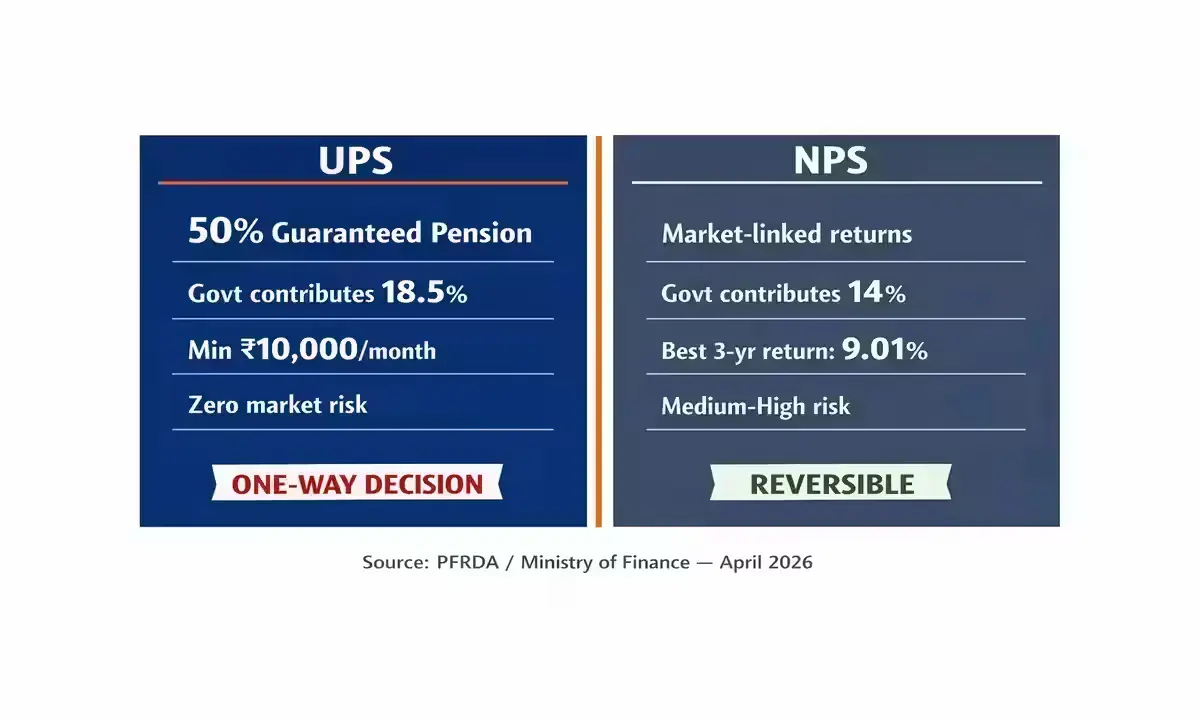

- The Unified Pension Scheme (UPS), operational from April 1, 2025, is the biggest Central Government pension reform since 2004 — and the opt-in decision is one-way and irreversible.

- Five states — Himachal Pradesh, Rajasthan, Chhattisgarh, Punjab, and Jharkhand — have independently restored OPS; no central-level restoration is confirmed.

- NPS AUM crossed ₹16.5 lakh crore as of February 2026, with best 3-year fund returns of 9.01% (LIC PF Fund / UTI PF Fund).

- Private options — LIC New Jeevan Shanti, HDFC Smart Pension Plus, ICICI Pru Guaranteed Pension Plan — offer guaranteed lifelong annuities with zero market risk, at a higher entry cost.

Source: PFRDA, PIB, verified April 24, 2026.

Why India’s Pension System Is More Fragmented Than You Think — And Why That’s Your Problem

Most retirement planning articles in India describe pension schemes in isolation. That is the wrong lens. India’s pension system in 2026 is a patchwork of seven distinct architectures, each with different guarantees, contribution structures, tax treatments, and exit rules.

The foundational divide: India runs two types of pension systems simultaneously. Defined Benefit (DB) schemes — like OPS and UPS — promise a fixed, formula-based pension regardless of market conditions. The government bears the investment risk. Defined Contribution (DC) schemes — like NPS and EPF — accumulate a corpus based on contributions and returns. The subscriber bears the risk, partially or fully.

The Union Cabinet approved the Unified Pension Scheme on August 24, 2024, with an assured pension of 50% of average basic pay drawn over the last 12 months prior to superannuation for minimum qualifying service of 25 years — and a minimum assured pension of ₹10,000 per month after at least 10 years of service. This was designed to address the instability NPS created for government employees after years of union pressure.

The State-level rupture: The Central Government moved to NPS in 2004. But after two decades, OPS has been re-implemented in Himachal Pradesh, Rajasthan, Chhattisgarh, Punjab, and Jharkhand — each driven by election mandates. The RBI warned in its State Finances bulletin that OPS restoration creates long-term fiscal liabilities, particularly when NPS recruits from 2004–2024 begin retiring from 2034 onwards.

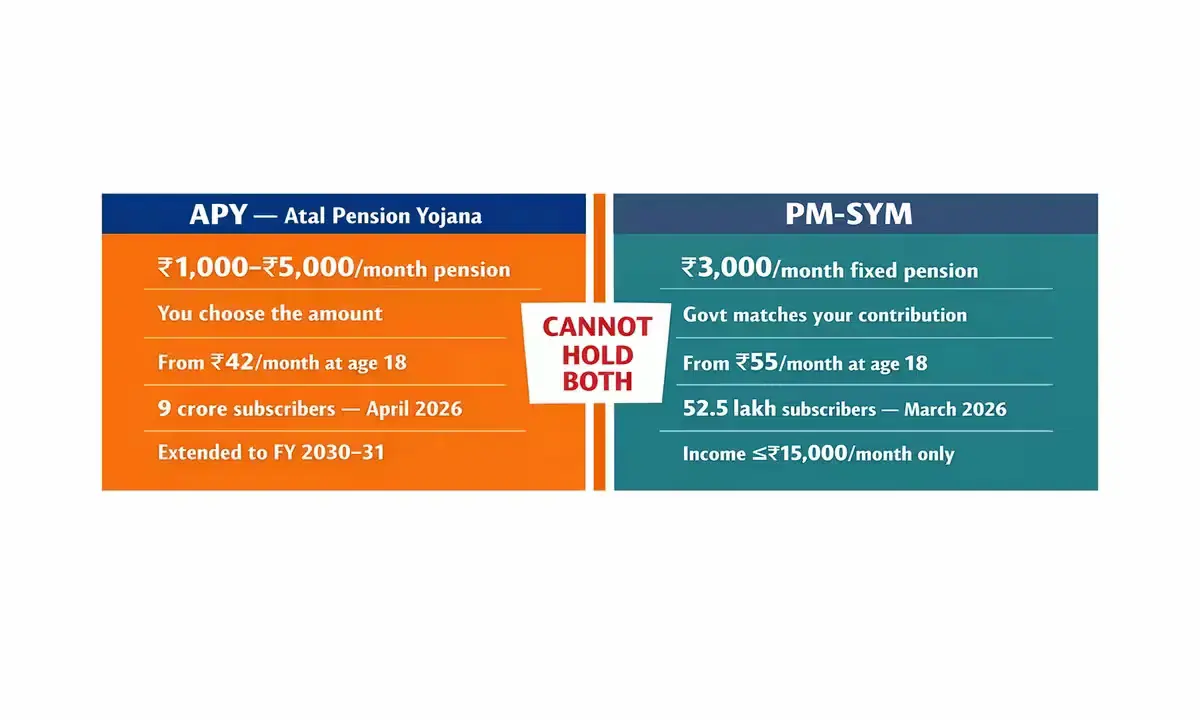

The unorganized worker crisis: India has over 450 million unorganised-sector workers. They have two government-backed options in 2026: APY (₹1,000–₹5,000/month) and PM-SYM (fixed ₹3,000/month). Combined, they cover fewer than 9.5 crore subscribers — roughly 21% of the eligible population.

Source: PM India Cabinet Approval, PFRDA, RBI State Finances Report, verified April 24, 2026.

Every Major Pension Scheme in India Right Now — April 2026 Status Check

As of April 24, 2026, here is the verified live status of every major pension scheme across all three sectors.

Central Government Schemes

Unified Pension Scheme (UPS)

Live Apr 2025

Central Govt

Central Government employees receive a guaranteed pension of 50% of their average basic pay over the previous 12 months, with at least 25 years of service. Government contributes 18.5% of basic pay + DA. Employee contributes 10%. Minimum guaranteed: ₹10,000/month after 10 years. Family pension: 60% of subscriber’s pension.

National Pension System (NPS)

Live — All Citizens

Market-linked. NPS AUM exceeded ₹16,50,000 crore as of February 2026 with ~2.2 crore subscribers. Tax benefits: up to ₹1.5 lakh under Section 80C + ₹50,000 under 80CCD(1B). At retirement (age 60), 60% lump sum tax-free; 40% must purchase annuity. Best 3-year NPS fund return: 9.01% (LIC PF Fund / UTI PF Fund, January 2026).

Atal Pension Yojana (APY)

9 Crore Subscribers

For non-ITR filers aged 18–40. ₹1,000–₹5,000/month guaranteed pension from age 60. Minimum: ₹42/month (age 18). Extended to FY 2030–31 (Cabinet, January 2026). Full details: Atal Pension Yojana 2026 complete guide.

PM-SYM (Pradhan Mantri Shram Yogi Maandhan)

52.5 Lakh Enrolled

Over 52.5 lakh people enrolled as of March 2026. Fixed ₹3,000/month pension from age 60. Contributions: ₹55–₹200/month, matched rupee-for-rupee by the Government. Only for unorganised workers earning ≤₹15,000/month who are NOT EPFO/ESIC/NPS members.

NPS Vatsalya

Live — For Minors

Contributory pension scheme for minors, managed by parent/guardian until the child turns 18, then converts to a standard NPS Tier-I account. Minimum: ₹1,000/year. All NPS tax benefits apply to parent’s contribution under Section 80C.

State Government Schemes

Old Pension Scheme (OPS)

5 States Only

Non-contributory (zero employee contribution). Pension: 50% of last drawn basic pay, with Dearness Relief, for life. Currently operational in Himachal Pradesh, Rajasthan, Chhattisgarh, Punjab, and Jharkhand for state employees. Central Government has NOT restored OPS — the UPS is the Central Government’s answer.

NPS — State Level

Most States

All states except the five OPS-restored states continue NPS for employees recruited after 2004. Uses the same PFRDA architecture as Central NPS. Maharashtra was the first state to implement UPS (adopted August 25, 2024) for state employees — others may follow.

Private Sector Schemes

Employee Pension Scheme (EPS) — EPFO

Mandatory

Mandatory for all EPFO members. Employers contribute 8.33% of wages to EPS + 1.16% from Central Government. Pension payable after minimum 10 years of eligible service at age 58. Formula: (Pensionable Salary × Service Years) ÷ 70. Early pension option from age 50 with reduction.

LIC New Jeevan Shanti

Private — LIC

Single premium deferred annuity. Guaranteed lifelong income. Joint life or single life options. No medical exam required. Annuity payout: monthly, quarterly, half-yearly, or yearly. Available online and offline. Ideal for lump-sum conversion of retirement corpus into guaranteed income.

HDFC Life Smart Pension Plus

Private — HDFC

Single plan offering both immediate and deferred annuity. Options: life annuity, joint life, and return of premium on death. Flexible payout: monthly, quarterly, half-yearly, or yearly. Backed by HDFC Life’s AUM of ~₹3 trillion and solvency ratio of 194% (IRDAI minimum: 150%).

ICICI Pru Guaranteed Pension Plan

Private — ICICI Pru

Single-premium annuity. Guaranteed lifelong income. Choose immediate or deferred payouts (1–10 years deferment). Minimum annuity: ₹12,000/year (₹1,000/month). 11 annuity options. Online + Loyalty Booster offers 1% higher annuity rate.

Verified at pfrda.org.in, financialservices.gov.in, and epfindia.gov.in, April 24, 2026.

India’s Pension Schemes 2026 — The Full Comparison You’ve Been Looking For

| Scheme | Sector | Who Can Join | Monthly Pension | Contribution | Risk | Guaranteed? |

|---|---|---|---|---|---|---|

| UPS | Central Govt | Central Govt employees (NPS members) | 50% avg basic pay (min ₹10,000) | 10% + 18.5% Govt | Zero | ✅ Yes — Govt |

| NPS | Central/All | All Indians, age 18–70 | Market-linked (varies) | Flexible (min ₹500/yr) | Medium–High | ❌ No |

| APY | Central Govt | Non-ITR filers, age 18–40 | ₹1,000–₹5,000 | ₹42–₹1,454/month | Zero | ✅ Yes — Govt |

| PM-SYM | Central Govt | Unorganised, income ≤₹15,000, age 18–40 | ₹3,000 (fixed) | ₹55–₹200 (govt matches) | Zero | ✅ Yes — Govt |

| NPS Vatsalya | Central Govt | Minors (via parent/guardian) | Market-linked (converts at 18) | Min ₹1,000/year | Medium | ❌ No |

| OPS | State Govt (5 states) | State Govt employees (OPS states only) | 50% of last drawn pay | Zero | Zero | ✅ Yes — State |

| NPS (State) | State Govt | State Govt employees (non-OPS states) | Market-linked | 10% basic pay | Medium–High | ❌ No |

| EPS (EPFO) | Private | EPFO members, 10 yrs+ service | Salary × yrs ÷ 70 | 8.33% employer + 1.16% Govt | Low | ✅ Yes — formula |

| LIC Jeevan Shanti | Private (LIC) | All Indians, any age | Depends on corpus | Single premium lump sum | Zero | ✅ Yes — LIC |

| HDFC Smart Pension Plus | Private (HDFC) | All Indians, any age | Depends on corpus | Single/deferred premiums | Zero–Low | ✅ Yes — HDFC |

| ICICI Pru Guaranteed Pension | Private (ICICI) | All Indians, min age ~30 | Min ₹1,000/month | Single premium lump sum | Zero | ✅ Yes — ICICI Pru |

Frequently Asked Questions – Pension Schemes India 2026

The Decision Grid — Which Pension Scheme Is Right for You in 2026?

Match your profile to the right primary scheme, supplement, and immediate action.

| Your Profile | Best Primary Scheme | Best Supplement | Critical Action | Official Portal |

|---|---|---|---|---|

| Central Govt (25+ yrs) | UPS — 50% guaranteed pension | NPS Tier-II (voluntary savings) | Check UPS eligibility NOW — switch is irreversible | enps.nsdl.com |

| Central Govt (<10 yrs) | NPS — model returns before switching | Corporate NPS top-up | Do NOT switch to UPS without 25-year projection | pfrda.org.in |

| State Govt (OPS state) | OPS — zero contribution, 50% of last pay | PPF / NPS Tier-II | Verify your state’s OPS gazette notification | Your State DoPPW Portal |

| State Govt (NPS state) | NPS | UPS (if your state adopts) | Track your state’s UPS adoption announcement | pfrda.org.in |

| Private Salaried (EPFO) | EPS (mandatory) + NPS (voluntary) | LIC / HDFC annuity at retirement | Ensure 10 years of EPS service for pension | epfindia.gov.in |

| Self-Employed / Freelancer | NPS All-Citizen Model | LIC New Jeevan Shanti (at retirement) | Open NPS Tier-I for 80CCD(1B) ₹50,000 deduction | enps.nsdl.com |

| Unorganised Worker (≤₹15,000/month) | APY (₹1,000–₹5,000) OR PM-SYM (₹3,000 fixed) | Cannot hold both — choose one | For ₹3,000 pension: PM-SYM costs less. For ₹5,000: only APY | APY Portal / maandhan.in |

| Parent (for minor child) | NPS Vatsalya | APY (when child turns 18) | Start early — corpus compounds 40+ years | npstrust.org.in |

| High-Income (ITR filer) | NPS + Private Annuity | HDFC Smart Pension Plus / ICICI Pru Guaranteed | Ineligible for APY/PM-SYM — NPS + annuity is your stack | hdfclife.com |

| Cost to Enrol — All Govt Schemes | FREE — contribution amounts as specified per scheme above | |||

Finance — newshours18

Pravin covers government pension schemes, social security policy, and personal finance for India’s unorganised sector workers, tracking PFRDA, EPFO, and Ministry of Finance notifications directly from official sources.