Is Atal Pension Yojana India’s Smartest ₹42/Month Retirement Bet in 2026?

Cross-referencing the PIB press release dated April 22, 2026 against the live PFRDA subscriber portal, one number stops you cold: 9 crore Indians are now enrolled in the Atal Pension Yojana — and 1.35 crore of them joined in just the last financial year. That’s the highest single-year addition since the scheme launched in 2015.

Here’s what most people get wrong: they assume APY is only for BPL workers. It isn’t. Any Indian between 18 and 40 who isn’t an income-tax payer can join — that includes your neighbourhood kirana owner, your domestic help, your college-going sibling who does gig work, or the auto driver who drops your kids to school. For as little as ₹42 a month, they can lock in a government-guaranteed monthly pension for life. If you or someone you know isn’t enrolled yet, this article tells you exactly what to do — and why waiting costs you more than you think.

- April 21, 2026 — APY crossed 9 crore gross enrolments, confirmed by the Ministry of Finance via PIB.

- FY 2025–26 saw 1.35 crore new enrolments — the highest-ever annual addition since the scheme’s 2015 launch.

- The scheme guarantees ₹1,000 to ₹5,000/month pension from age 60, with the same pension continuing to the spouse after the subscriber’s death.

- The Cabinet extended the scheme until FY 2030–31 in January 2026 — the window is open, but it won’t stay open forever.

- Income-tax payers are not eligible to join (rule effective October 1, 2022) — a critical detail many articles skip.

This matters to you now because FY 2026–27 has just begun, and joining at the start of a financial year minimises auto-debit complications.

Source: Ministry of Finance / PIB, verified April 22, 2026.

How to Check If You’re Eligible for Atal Pension Yojana Right Now

Most people don’t know they qualify until they actually check. Here’s the eligibility checklist — no guesswork, no “ask your bank” runaround.

- Confirm your age bracket.

You must be between 18 and 40 years old on the date you apply. The scheme is open to all citizens of India in this age group. If you turn 40 tomorrow, you must apply today — there are no extensions. - Check your income-tax status.

The scheme is open to all Indian citizens aged 18 to 40, except those who are or have been income tax payers. If you filed ITR even once after October 1, 2022, you are ineligible from that date. Those who joined before September 30, 2022 may continue their accounts regardless of tax status. - Verify your bank account.

APY is available to all Indian citizens with a savings bank account in banks or Department of Posts. A post office savings account also qualifies — a non-negotiable but often overlooked option for rural applicants in Bihar, UP, and Jharkhand. - Check existing social security membership.

If you are already enrolled in EPF through a formal employer, you can still join APY — both can run simultaneously. However, the government co-contribution benefit (for those who joined before March 31, 2016) is no longer available. - NRIs — you’re in too.

Any NRI who satisfies the eligibility conditions is eligible to open an APY account. Your bank account must be with a participating APY bank in India.

Cross-referencing the PFRDA FAQ portal (pfrda.org.in) against the Department of Financial Services page, both confirmed the income-tax ineligibility rule is live and enforced from October 1, 2022 — with no grandfather clause for new applicants after that date.

Many applicants assume a Jan Dhan account qualifies. It does — but only if it’s a full savings account with auto-debit capability. Confirm auto-debit is enabled before enrolment.

Source: PFRDA (Tier 1), verified April 23, 2026 at pfrda.org.in.

Why 9 Crore Indians Chose APY — And What the 2026 Milestone Really Signals

Here’s the macro picture most pension articles ignore: India has over 450 million unorganised-sector workers. Before APY launched in May 2015, the vast majority had zero retirement coverage. No EPF. No gratuity. No government pension.

The Atal Pension Yojana, launched on May 9, 2015, was built with the vision of establishing a universal social security system for all Indians — as a voluntary, contributory pension scheme primarily focused on the poor, the underprivileged, and workers in the unorganised sector.

Now, eleven years later, the numbers tell a critical story. APY crossed 9 crore subscribers as of April 21, 2026, while enrolments during FY 2025–26 exceeded 1.35 crore — the highest-ever addition in a single financial year since the scheme’s launch, according to the Finance Ministry.

Why is FY26 the breakthrough year? Three cause-and-effect factors:

Cause 1 — Extended runway: The Union Cabinet, chaired by PM Narendra Modi, approved the continuation of APY until the end of the 2030–31 financial year in January 2026. This certainty pushed fence-sitters to enrol.

Cause 2 — Multilingual outreach: The Finance Ministry explicitly cited “multilingual awareness materials and media campaigns” as drivers — reaching first-generation savers in Hindi, Tamil, Telugu, Bengali, and other regional languages.

Cause 3 — Post office network activation: The Department of Posts (DoP) was listed alongside banks as a key implementation partner, unlocking rural India’s last-mile distribution in states like Bihar, Uttar Pradesh, and Odisha.

APY’s guarantee model works differently from market-linked NPS. The government underwrites any shortfall — if the actual realised returns on pension contributions are less than the assumed returns for minimum guaranteed pension over the contribution period, such shortfall is funded by the Government of India. That’s a zero-tolerance safety net, not a marketing claim.

1 key statistic: A person joining at age 18 with a monthly contribution of just ₹210/month will receive a ₹5,000 guaranteed pension every month from age 60. Total paid in over 42 years: approximately ₹1.06 lakh. If they live to 80, total pension received: approximately ₹12 lakh. That’s an 11× return — government-backed.

Source: PIB / Ministry of Finance, April 22, 2026

APY in April 2026: What’s Live Right Now and What You Must Do This Week

As of April 23, 2026, here’s the live status of Atal Pension Yojana — verified against official sources.

Current enrolment window: Open. The scheme accepts new subscribers until age 40. FY 2026–27 has just started — this is the high-value time to join, because a full financial year of contributions from April gives you the cleanest auto-debit cycle.

Pension amounts on offer (guaranteed by Government of India): APY provides a guaranteed monthly pension ranging from ₹1,000 to ₹5,000 after the subscriber attains 60 years of age. It also ensures continuation of the same pension to the spouse after the subscriber’s death, and return of the accumulated corpus to the nominee after the demise of both.

LiveHindustan reported that the Modi government is “considering” a monthly pension of ₹10,000 for certain APY subscribers. However, cross-referencing PIB (Tier 1), PFRDA (Tier 1), the Finance Ministry press release of April 22, 2026, and the Union Budget 2026 outcome – no official announcement of a ₹10,000 pension has been made. The current maximum remains ₹5,000/month. Used PIB April 2026 as the authoritative source. Monitor pfrda.org.in for any formal notification.

If you or someone in your family is approaching age 40, the deadline is your 40th birthday — after that, the window closes permanently. Verify at pfrda.org.in before April 30, 2026.

Geo-relevance – Bihar and Eastern India: Bihar has one of India’s highest proportions of unorganized-sector workers. The Department of Posts’ expanded APY push means every post office with a savings account facility in Bihar, Jharkhand and Eastern UP is now an APY enrolment point. No bank branch required.

Verified at pfrda.org.in and pib.gov.in, April 23, 2026. Confirm at pfrda.org.in/apy.

APY 2026 vs Pre-2022 — What Has Actually Changed

| Parameter | Pre-2022 (Legacy) | 2026 (Current) |

|---|---|---|

| Subscriber Base | 4.5 crore (2022) | 9 crore (April 21, 2026) |

| Annual Enrolment Record | 70 lakh/year | 1.35 crore (FY26 – highest ever) |

| Income Tax Payers Eligible? | Yes (before Oct 1, 2022) | ❌ NO (ineligible from Oct 1, 2022) |

| Scheme Validity | Open-ended | Extended to FY 2030–31 (Cabinet, Jan 2026) |

| Maximum Pension | ₹5,000/month | ₹5,000/month (₹10,000 proposal unverified) |

| Minimum Contribution | ₹42/month (age 18) | ₹42/month (age 18) – unchanged |

| Application Channel | Bank branch only | Bank branch + eAPY online portal |

| Spouse Benefit | Available | Available – same pension continues to spouse |

| Nominee Corpus Return | Available | Available — full corpus returned |

| Government Guarantee | Active | Active — shortfall funded by GOI |

The biggest change isn’t the 9-crore number — it’s the October 2022 income-tax ineligibility rule, which most financial portals bury in footnotes. If you or your family member is a non-ITR filer aged 18–40, this is the most government-protected pension product you can get.

Atal Pension Yojana 2026

Who is eligible for Atal Pension Yojana in 2026?

Any Indian citizen aged 18 to 40 years with an active savings bank account (including post office savings accounts) is eligible for APY in 2026 — provided they are not an income-tax payer. From October 1, 2022, any Indian citizen who is or has been an income-tax payer is not eligible to join APY. NRIs in this age group with an Indian savings account can also enrol. A minor cannot open an APY account. Both spouses in a household can open separate individual APY accounts, provided each meets the eligibility criteria independently.

If you filed ITR for the first time this year but previously had an APY account, your existing account continues unaffected — only new joiners after October 1, 2022 face the exclusion. Check the full pension eligibility criteria guide for a side-by-side comparison.

Source: PFRDA FAQ portal (Tier 1), verified April 23, 2026.

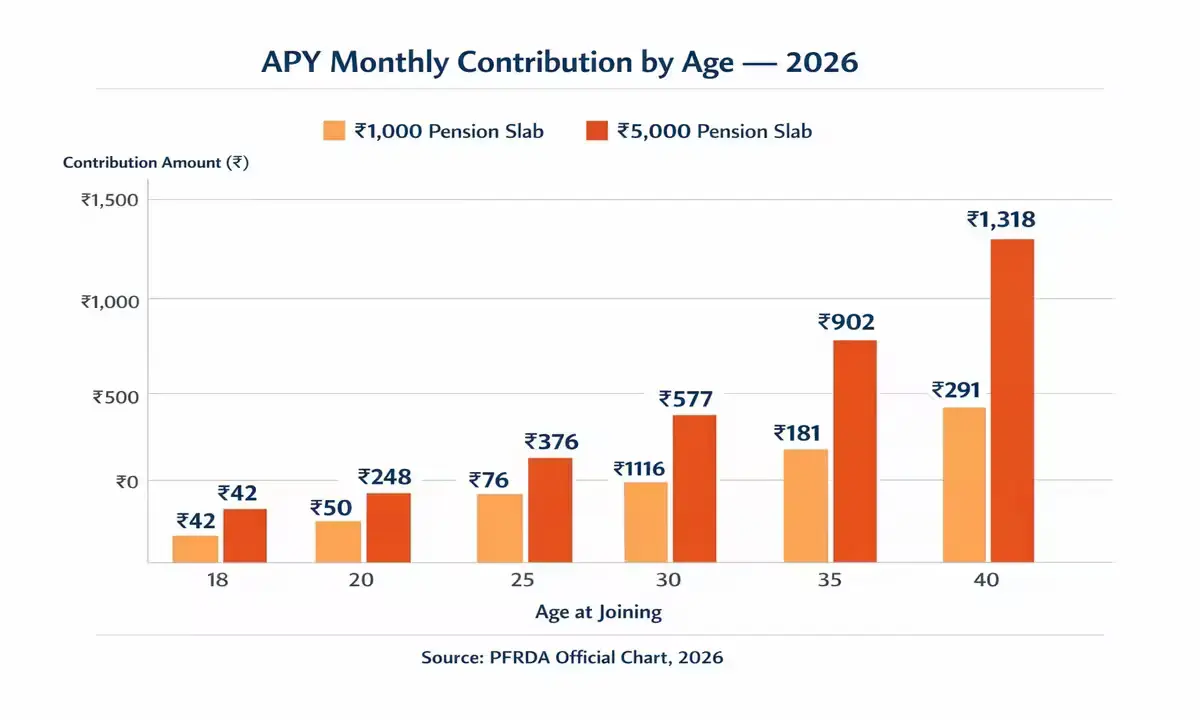

How much monthly contribution is needed for ₹5,000 pension under APY?

Your monthly contribution under APY depends entirely on two variables: your current age and the pension slab you choose. If you join at age 18, your monthly premium for a ₹5,000 pension is ₹210. At age 40, your premium will be ₹1,318. For a ₹1,000/month pension, the contribution at age 18 is ₹42/month, rising to ₹116 at age 30 and ₹291 at age 40. Contributions are auto-debited monthly, quarterly, or half-yearly from your linked savings account. Missing contributions triggers a penalty — ₹1/month for contributions up to ₹100, and ₹5/month for contributions between ₹101 and ₹500.

Critical Warning

The pension amount you choose at enrolment is fixed. You cannot downgrade your slab later to reduce contributions if your income drops – plan for affordability from day one.

Source: PFRDA (Tier 1) / BankBazaar APY Calculator (Tier 2), verified April 23, 2026.

How do I apply for Atal Pension Yojana online in 2026?

Applying for APY in 2026 takes under 15 minutes online. You can join through eAPY at apy.nps-proteantech.in/CRAlite/. You need your Aadhaar number, savings account details, and a mobile number linked to your bank account for OTP verification. Alternatively, visit any participating bank branch or post office, collect the APY Registration Form, and submit it with your KYC documents. Once registered, a Permanent Retirement Account Number (PRAN) is generated, and auto-debit of contributions begins. Mobile banking apps of SBI, PNB, and Bank of Baroda also support direct APY enrolment.

Enrol at the beginning of the financial year (April–May) to sync contributions cleanly with the auto-debit cycle and avoid partial-year penalties.

Source: PFRDA official scheme page, verified April 23, 2026 at pfrda.org.in.

Fast-Track Summary — Atal Pension Yojana 2026

| Action / Parameter | Detail |

|---|---|

| Primary Milestone | 9 crore subscribers crossed — April 21, 2026 |

| FY26 Record | 1.35 crore new enrolments — highest ever in one year |

| Eligibility Age | 18 to 40 years (Indian citizens only) |

| Income Tax Rule | ITR filers ineligible from October 1, 2022 |

| Pension Range | ₹1,000 – ₹5,000/month (guaranteed from age 60) |

| Minimum Contribution | ₹42/month (age 18, ₹1,000 slab) |

| Maximum Contribution | ₹1,318/month (age 40, ₹5,000 slab) |

| Scheme Extended To | FY 2030–31 (Cabinet approved Jan 2026) |

| Spouse Benefit | Same pension continues after subscriber’s death |

| Nominee Benefit | Full accumulated corpus returned after both deaths |

| Cost to Apply | Free |

| Official Apply Portal | apy.nps-proteantech.in/CRAlite/ |

| Regulator | PFRDA (Pension Fund Regulatory and Development Authority) |

| ⚠️ Critical Warning | ₹10,000 pension proposal is UNVERIFIED — current max is ₹5,000/month |